Barriers Preventing Raw Cashew Exporters from Moving Up the Value Chain

Limited Processing Capacity and Infrastructure

Many raw cashew-producing countries lack modern processing facilities and sufficient installed capacity. As a result, the proportion of locally processed cashews remains low, with many factories underutilised or inactive. For example, Tanzania has 57 cashew processing plants, but only 36 are operational, with a combined installed capacity of 103,395 tons—far below the country’s raw cashew production. Cambodia also needs at least 50 new medium-sized facilities to meet its 2027 processing targets.

Additionally, inadequate post-harvest storage and handling infrastructure lead to significant losses and quality degradation, making raw nuts unsuitable for further processing. This affects local processors’ ability to accumulate sufficient quality raw materials.

This infrastructure limitation is a dynamic rather than static issue. When capacity is lacking, raw cashews are exported, reducing the incentive to invest in domestic processing. This creates a vicious cycle where limited infrastructure sustains raw exports, hindering the development of a strong local processing industry. If raw materials deteriorate due to improper handling, they become less attractive for processing, further weakening incentives.

Limited Access to Capital and Financing

Local processors often struggle to secure working capital to purchase raw cashews, especially when competing against well-financed foreign buyers. Initial capital requirements for building a processing plant and acquiring raw materials are substantial. For example, in Tanzania, constructing a 4,000-ton/year facility can cost $1.5 million, plus $3.1 million for raw material procurement.

Local financial institutions tend to avoid lending to cashew processors, perceiving them as high-risk borrowers with low repayment capacity. This hesitation creates a key bottleneck. Combined with the ability of foreign buyers to offer instant cash or higher prices, it distorts the market. Underfunded local processors are unable to compete, even with policies like “local processor purchasing priority,” highlighting a systemic failure of financial markets to support local value addition.

Outdated Technology and Equipment

Many African processors still rely on manual or semi-mechanised tools with limited capacity, resulting in sub-optimal product quality and poor global competitiveness. This contrasts sharply with Vietnam’s efficient processing techniques and modern roasting methods.

Upgrading to efficient modern processing equipment is urgently needed, but it requires significant investment. Dependence on imported machinery can also introduce logistical complications, higher costs, and supply chain disruptions.

Obsolete technologies directly affect kernel quality, such as higher breakage rates or inconsistent output. This makes it difficult for local processors to meet strict international quality standards (e.g., moisture content, defects, pesticide residues, aflatoxin) and certifications (ISO, HACCP, Fair Trade, Organic). Hence, the technology gap is a fundamental barrier to market access and profitability.

High Operating Costs

While some producer countries like Tanzania have very low minimum wages ($0.10/hour), overall labour productivity may be significantly lower (e.g., Tanzania is 30% less productive than India). This means that despite low wages, per-unit costs remain high due to inefficiency.

High energy costs are also a major factor. Tanzania’s energy costs are 2–3 times higher than Vietnam’s, pushing processing costs up (e.g., $150/ton in Tanzania vs. $70/ton in Vietnam).

Logistical and transportation costs are additional challenges. Transporting raw cashews is inefficient (5 containers of raw nuts produce 1 container of kernels). In countries like Vietnam, logistics costs remain high (about 16.8% of GDP), due to port congestion, container shortages, and high shipping rates. However, processing closer to the source (in Africa) may be cheaper for delivery to Europe/US compared to shipping raw nuts to Asia first.

Even with abundant raw materials, high operating costs (energy, inefficient labor, logistics) can eliminate the advantages of local production. This makes it cheaper for international buyers to import raw nuts and process them in more efficient economies (like Vietnam), despite longer transport distances. This creates a “cost-competitiveness trap” for producer nations, rendering local value addition economically unfeasible without major efficiency improvements.

Unfavourable Policy and Regulatory Environment

Many producing countries have introduced policies to promote local processing (e.g., export taxes on raw nuts, kernel subsidies, tax holidays, investment zones, raw material prioritisation for local processors). However, some reports indicate that these policies often fail to deliver the desired outcomes. In Tanzania, the export tax on raw cashews (15% of FOB price or $160/ton) has not significantly boosted local processing, and only a small portion of tax revenue is reinvested in the industry.

Issues like smuggling and informal trade further affect local processors’ access to raw materials. For instance, raw nuts are smuggled from Côte d’Ivoire to Burkina Faso/Guinea-Bissau and from Benin to Togo, undermining domestic processing by diverting raw materials. This is often driven by higher prices in informal markets or laxer regulations.

Export taxes (like Tanzania’s 15%) are intended to encourage domestic processing. But if they’re poorly enforced, not reinvested, or easily bypassed through smuggling, they become ineffective—or even counterproductive. This underscores the difficulty of designing policies that effectively shift market behaviour toward value addition without introducing new distortions.

Market Dynamics and Competition

The dominance of established processing hubs is a major barrier. Vietnam and India together process 93% of the world’s cashews, with Vietnam being the largest processor and exporter of kernels. These countries benefit from economies of scale, well-established supply chains, and strong market access.

Producer countries also struggle to meet strict international standards and market entry requirements for processed kernels. They face challenges meeting quality benchmarks (e.g., moisture, defects, pesticide residues, aflatoxin) and certifications (ISO, HACCP, Fair Trade, Organic) required by major importing markets like the EU and US.

The long-standing dominance of Vietnam and India has created a significant “first-mover advantage.” They control distribution networks, have established buyer relationships, and possess the infrastructure and expertise needed. This entrenched position makes it extremely difficult for new entrants from raw cashew-producing countries to gain market share, even if they overcome local processing challenges. This represents a classic entry barrier in global value chains.

Summary of Government Incentives for Cashew Processing in Major Producing Countries

Vietnam’s Dominance in Cashew Processing

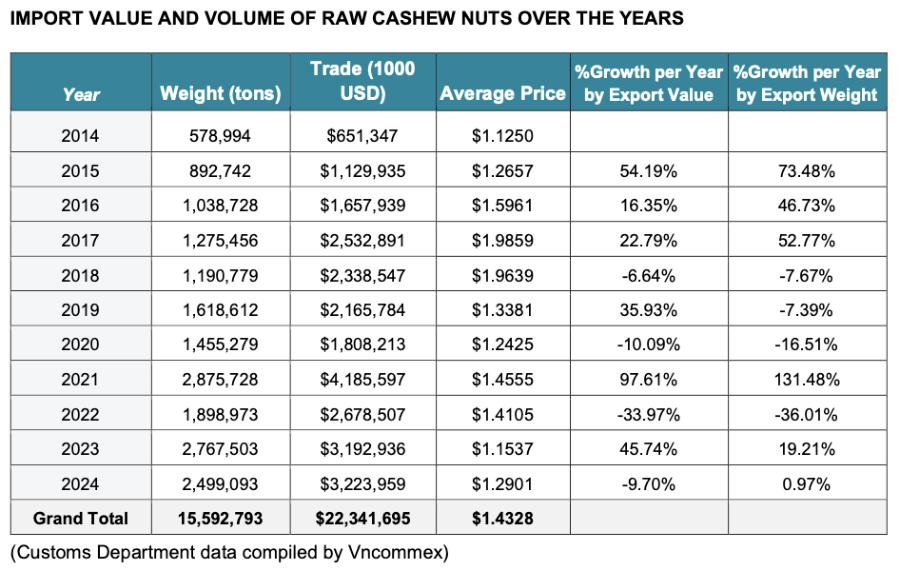

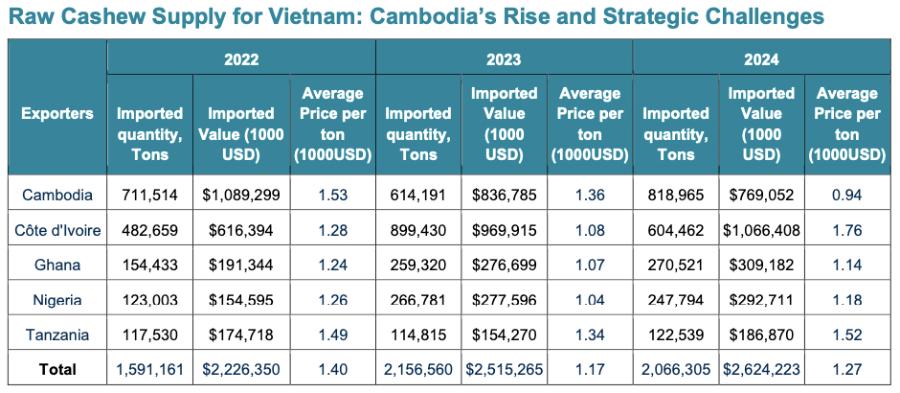

Vietnam has maintained its position as the world’s leading exporter of processed cashew kernels for 18 consecutive years, accounting for over 80% of global kernel exports. Remarkably, this achievement has been made despite Vietnam importing most of its raw cashew materials, primarily from Africa and Cambodia.

See more of the analysis of the Cashew nuts industry here: CASHEW NUTS IMPORT & EXPORT MARKET 2025 REPORT

Key factors behind Vietnam’s success include:

- Investment in modern processing technology: Vietnam has adopted efficient processing technologies that deliver high-quality kernels at competitive costs.

- Skilled labour and operational efficiency: Vietnam can process large volumes efficiently, reflecting skilled labour and optimised operations.

- Strong market access and diversification: Vietnam has diversified beyond the U.S. to markets like China and the EU, benefiting from trade agreements like EVFTA, which reduces EU kernel import tariffs to 0%.

- Strategic raw material sourcing: Vietnam’s ability to import from various sources ensures a steady supply for its processing industry, even when domestic output fluctuates.

- Cost efficiency (despite high logistics costs): Despite logistics costs accounting for 16.8% of GDP, Vietnam maintains its dominance through overall processing efficiency and competitive pricing.

Vietnam’s success is not based on raw material self-sufficiency but on its ability to coordinate the global cashew value chain efficiently. It capitalises on processing capacity, market access, and strategic sourcing to capture the most profitable segment, turning its raw material deficit into a competitive advantage. This offers a strategic model for other countries: become a processing hub, even if it means importing raw nuts.

See more of the analysis of the Cashew nuts industry here: CASHEW NUTS IMPORT & EXPORT MARKET 2025 REPORT

Opportunities for Countries with Large Cashew Resources

Opportunities for Countries with Large Cashew Resources

The “cashew paradox” persists due to a complex mix of capital constraints, technological gaps, labor shortages, high operational costs, and inconsistent policies in raw cashew-producing countries. However, the economic benefits of local value addition—including foreign exchange earnings, job creation, and economic diversification—are substantial and represent a critical path to sustainable development.

Shifting from raw exports to processed kernel exports is not just an economic choice, but a strategic imperative for these countries to move up the global value chain, enhance resilience, and secure a more prosperous future for their farmers and cashew sectors. Learning from successful models like Vietnam—combined with tailored domestic strategies and international partnerships—is key to unlocking this untapped potential.

Conclusion

Vietnam currently sits at the pinnacle of the global cashew value chain—but that position is not guaranteed forever. As raw cashew-producing countries begin focusing on building domestic processing capacity, investing in modern technology, and improving policy environments, Vietnam’s role as the “global processing hub” may face increasing challenges in the near future.

However, the current gaps in technology, capital, labour, and supply chains remain significant obstacles for competitors. To maintain its edge, Vietnam must not rely solely on its current model—it needs to proactively upgrade its technology, restructure its supply chain for greater sustainability, and expand into high-value segments such as deep-processed products or organic cashews.

If done effectively, Vietnam can not only maintain its leadership but also reshape how the global cashew industry operates for decades to come.

Read more: Overview of Vietnam Cashew Market in the First 6 Months of 2025